Naked Put Study 2 (Part 7)

Posted by Mark on January 2, 2017 at 07:26 | Last modified: October 19, 2016 09:36What better way is there to break in the New Year than with new data? Today I continue analysis of naked put (NP) study 2 by studying the efficacy of stops.

I previously presented data comparing the naked put (NP) trade with long shares. This suggested outperformance by NPs. A drawdown analysis added complementary evidence. From there I went on to study the equity moving average as a potential filter for when to be in the trade. That was not encouraging.

Stop-losses are another potential means to improve the trade. Stops help avoid the largest losses at the cost of more frequent smaller ones. Stops result in trade exit, though, which shuts the window of opportunity for trade recovery (“whipsaw”). In theory, avoiding the most catastrophic of losses offers a better chance of long-term survival.

I therefore repeated NP Study 2 using end-of-day (EOD) stop-losses. Stop levels tested were multiples of the original credit. EOD implies the possibility of realizing a 4x loss even under a 2x stop condition (good future blog topic).

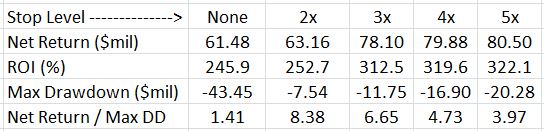

Let’s start with some vital statistics:

Return numbers are shown in the first two rows (not including header). The stops seemed to help. Net return without stops was the lowest. Looser stops (higher stop level) then resulted in greater returns.

Maximum drawdown (DD) is shown in the third row. No stops resulted in the largest max DD. Tighter stops resulted in the lowest max DD. This is precisely the reason stops are advertised.

Remember that DD helps to determine position sizing. I have written about this in terms of psychic pain. For these reasons, a system with lower DD is worth considering. I have a greater chance of sticking with such a system through tough times because I may not lose as much.

For these reasons, I included row 4 as a ratio of net return to maximum DD. It turned out the tighter (lower) the stop, the larger the ratio. Even the highest stop level has a ratio that is 2.8 times larger than using no stops at all.

I think this is huge.

Comments (1)

[…] particular, I noted the importance of the net-return-to-max-drawdown (DD) ratio. In looking at the 2x vs. 5x stop levels, for example, the difference in net return is not that big […]