Standard Deviation of Returns (Part 1)

Posted by Mark on December 11, 2017 at 07:12 | Last modified: September 10, 2017 15:03I have recently begun to trade a small friends-and-family account. In running the early numbers, I was surprised to see standard deviation (SD) of returns tracking higher for the portfolio than for the benchmark.

Based on my trading/research experience, naked puts (NP) generate comparable returns to the benchmark with a significantly lower SD of returns.

The best analysis I have between long shares and NPs may be the second graph shown here. In that analysis I did not calculate the total but using my naked eye and this online calculator, the NP portfolio returns 8.69% per year vs. 11.17% per year for the benchmark. That is not “comparable” returns—it’s a smackdown by the benchmark.

The graph does show this return comparison to be date sensitive. Just three months earlier (1.65% of the entire backtesting horizon), the NPs had a higher ROI than long shares. Across the whole graph, the NP line (red) beats long shares (blue) ~2/3 of the time. Statistically speaking, I worry about this inconsistency. Perhaps a rolling analysis should be done to get a larger sample size than just a single-point comparison, which may not be representative.

In the previous study I used maximum drawdown (MDD)—not SD of returns—as a measure of risk. When I looked at risk-adjusted return (RAR), the NP portfolio significantly outperformed despite the smackdown mentioned above.

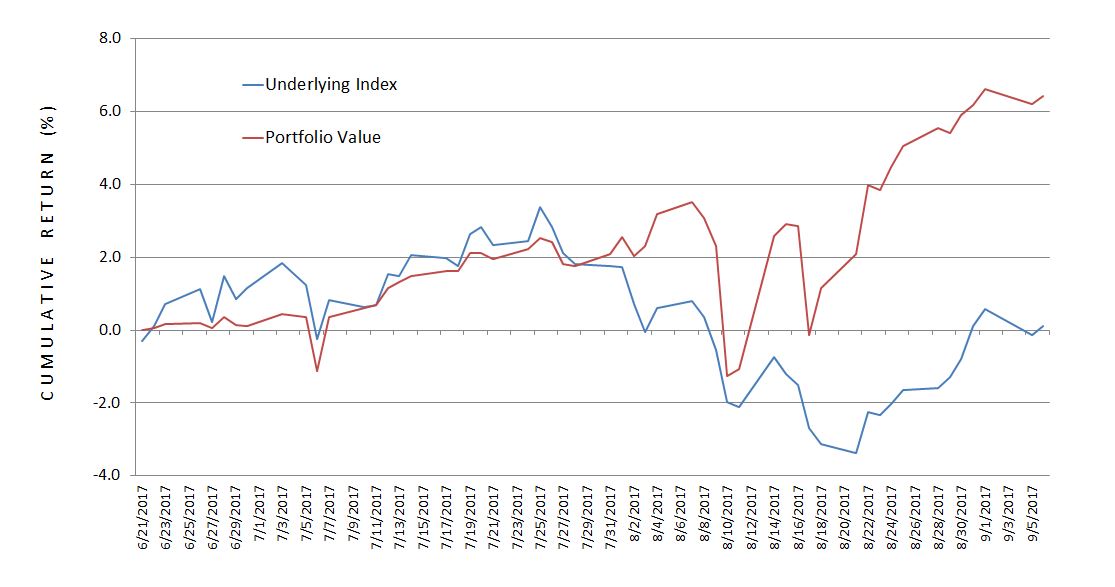

Now let’s move forward and study the NP portfolio I have been trading for 1/6 year. I track the cumulative return for the portfolio and for the underlying index:

This is consistent with what I have come to expect from NPs. The equity curves are similarly shaped. The underlying index or NPs can outperform when the market is higher or lower, respectively.

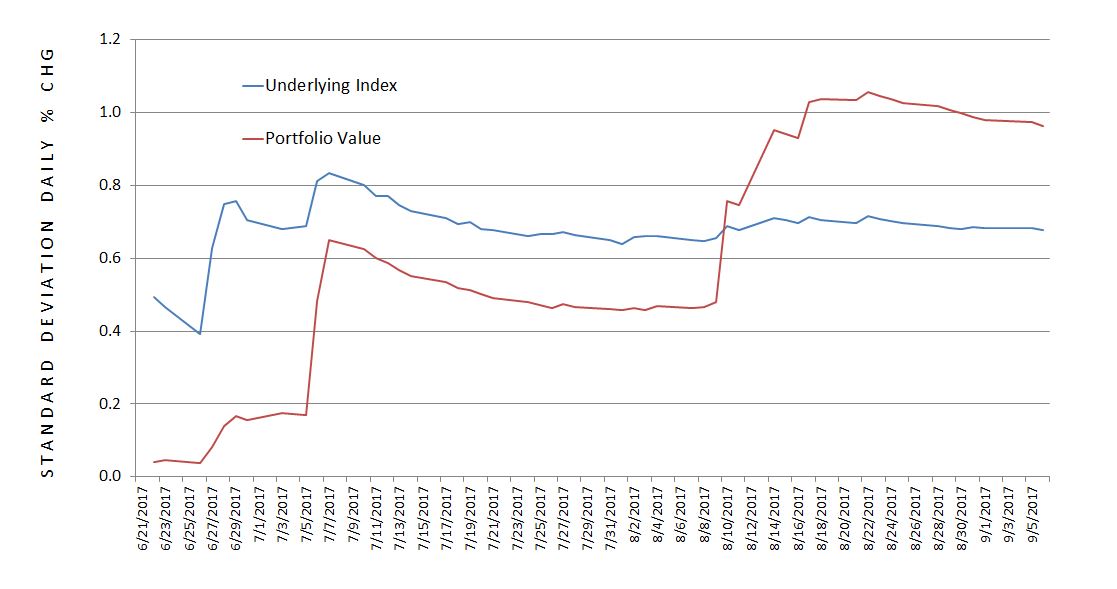

I calculate daily % returns so I can monitor the SD of both:

The NP portfolio shows a larger SD of returns than the benchmark! How can that be?

Categories: Money Management | Comments (1) | PermalinkOne Brief Paragraph

Posted by Mark on December 8, 2017 at 07:23 | Last modified: September 7, 2017 11:51On September 6, 2017, I met with a professor (now Dean) from my pharmacy school days for a career discussion. Today’s post is the fulfillment of two assignments.

First, he asked me to write one brief paragraph detailing what I seek from the business school and why.

I wish to speak with someone at Michigan Ross about the possibility of developing an affiliation with the school. Having worked as a trader in securities managing my personal account since 2008, such a relationship could enable me to:

- Give presentations about what I have learned during my non-traditional, hands-on journey

- Mentor students with an interest in the markets by working on specific data research and backtesting projects

- Facilitate networking with experienced trading professionals and/or fund managers nationwide

- Explore the possibility of transitioning my personal trading business into a wealth management firm for others

- Fulfill a New Years’ resolution to become more involved [with others]

Second, he asked me to write one brief paragraph detailing what I seek from the college of pharmacy and why.

I wish to give an investing presentation to Pharm.D. students and faculty. This could help to achieve several goals:

- Improve investment literacy: a subset of financial literacy especially relevant to professionals in higher-paying jobs

- Honor my pharmacy education, which included valuable critical-thinking lessons I consider to be largely responsible for my 10-year trading success

- “Give back” as an expression of gratitude for the business opportunity I feel lucky to have discovered during my sinuous academic and professional journey

- Gain valuable public-speaking experience

- Network with others who might have a desire to delve deeper into investment/financial education

Two detailed paragraphs in a shorter-than-average blog post… I hope this counts as being brief!

Meeting with XC (Part 3)

Posted by Mark on December 4, 2017 at 07:02 | Last modified: September 19, 2017 11:04Today I conclude with summarized notes from my meeting with financial adviser XC on August 22, 2017.

If I want to find people with a disproportionate equity concentration then XC suggested looking at Domino’s Pizza, headquartered locally, which has gone from $8 to $160 in recent years. Ford is another possibility (think of all the commuters going to Dearborn every day) along with DTE Energy and Consumers Energy.

XC is a believer in credentials: the more the better. Series 65 is the minimum requirement to manage money in Michigan but it’s given by FINRA, which is focused more on brokerages. He suggested looking into options/derivatives licenses as well.*

Hypothetically speaking, if he advised for one of my trading clients then I would be my own solo practitioner. He would not officially recommend me—doing so would put his company’s reputation at risk—but he would be interested in my performance. He would also be mindful of my fees. If I were generating a lot of short-term capital gains for a client with an annual capital gains budget then it might affect how he would manage their trading portion. The more fees I charge, the less the overall AUM, which would lower his compensation. This could be a potential conflict of interest.

If I were to pitch my trading strategy then XC said they would have to play devil’s advocate by addressing risk and liability exposure. I was not sure whether or not this was intended to be a hint.

XC recommends Schwab Advisor Services at >$5M AUM because of the useful tools they offer. At $25M AUM they pair you with a corporate relationship expert.

XC seemed like a sincerely nice person with a solid knowledge base. He was also generous with 100 minutes of his weekday time. If I start an IA then he said he would be interested to hear how I progress. If I need anything further then he invited me to call. He expressed interest in reading my blog and suggested again that I check out their website and available tools.

I took a few useful suggestions away from our meeting. I will make a LinkedIn profile. I will think more about putting together a presentation of my story and/or what I do. I will also look into whether any [insurance] companies might be looking for IAs to manage their cash position.

*–Series 3 is the National Commodities Future Examination and Series 4 is the Registered Options Principal Examination. I question the relevance of the former to trading options and I’m doubtful about the latter, which deals with supervising option traders and trading activity.

Categories: Networking | Comments (0) | PermalinkMeeting with XC (Part 2)

Posted by Mark on December 1, 2017 at 07:41 | Last modified: September 19, 2017 09:49I continue today with summarized notes from my meeting with financial adviser XC on August 22, 2017.

XC managed assets for an insurance company that grew to over $200M AUM through some fortuitous M/A activity. His first personal clients were co-workers who liked what he did with corporate funds and asked him to manage their money. This was $25M in a single-shot that he credits more to luck than he does to investing skill.

XC introduced me to E/O (errors and omissions) insurance. One example of an E/O situation is where the IA goes to buy 25,000 stock shares of stock for a client and accidentally enters the wrong ticker symbol. The IA would be liable for any losses and E/O insurance would protect the firm. I did not get the chance to ask about cost.

He talked a lot about some of the free tools located on his company’s website, which allow clients to make future growth projections and to see how their overall financial situation is progressing. He suggested I check out these tools and encouraged entry of some personal information to see what it says about me.

After discussing these tools for a few minutes I pointed out that trading, not financial planning, is what I want to do. Even so, he argued, I should not aim to be a trader who has no personal relationship with clients. Talking about their total financial plan and where I fit in is a way to avoid such anonymity that could otherwise leave clients’ future satisfaction solely dependent on my trading performance [“everyone knows” no strategy works well in all markets]. XC said client turnover is very costly in this industry because expenses to the firm are front-loaded.

Getting back to the website, XC said they post a blog every 2-3 weeks of 1,000 words or less. They rarely post market commentary because he doesn’t want content to be time-limited. He said the blog is a really good way to get an idea of how/what someone thinks. The posting date (although it may be changed or the post deleted) adds context about current events surrounding a stated viewpoint.

He attributes a lot of his success to networking. Some of his jobs arose because of people he knew as far back as college.

XC talked about a gynecologist he knew who later went into finance. He was interested in trading but didn’t want to be the one doing the trading. Instead he did extensive research on a broad spectrum of wealth managers and became an encyclopedia of available offerings in the industry. Combining this with his knowledge of physicians’ backgrounds and needs, he was able to talk to clients and make (give) relevant recommendations (advice).

I will conclude next time.

Categories: Networking | Comments (1) | PermalinkMeeting with XC (Part 1)

Posted by Mark on November 27, 2017 at 07:16 | Last modified: September 6, 2017 08:31On August 22, 2017, I met with a financial adviser to share my story, to learn about his, and to hear any ideas or suggestions he might have about transitioning my career toward the IA domain.

Although I have removed/changed his name (initials), I would feel comfortable recommending XC to anyone looking for a financial adviser. Please e-mail me if that might be you.

I was shocked to realize our meeting had lasted 100 minutes. XC was very generous with his weekday time.

As part of their service, XC’s firm trades securities for clients and he believes their edge is 25-50 basis points. For smaller net-worth clients they use ETFs. For larger net-worth individuals they use individual equities. They do a fair bit of covered call writing as a mechanism to defer capital gains taxes. On two occasions he mentioned an example where someone with a large equity position and low cost basis would trigger heavy capital gains upon sale.

I am very curious to know more about their trading edge. Does he believe in CCs as a mechanism for outperformance? Where did they procure their trading expertise? How were they trained? Do they make consistent efforts to improve? If so then how? I believe it’s important to remain focused on realistic returns but I would also recommend any self-directed investor to aim higher than 50 basis points.

XC believes the money management industry is a highly competitive space with a low barrier to entry. He estimates a start-up cost of $50K to start an IA—much higher than I would have guessed!—and significantly less on an ongoing, annual basis.

He thinks my best chance for success is to find people interested in my particular type of trading and/or what I offer. I asked if he thinks the average investor is educated enough to understand what I do and he said no: the average investor doesn’t really care much about how the IA generates returns. This struck me as contradictory: why try to find people interested in my type of trading if they can’t understand what I tell them?

XC recommended I subscribe to LinkedIn professional as a way to find others who share my niche expertise and interest. His preferred approach to networking is finding someone else who knows the target and asking that person to refer me.

He also suggested I speak with the Ross School of Business (daughter’s alma mater) to find others working on related [option trading] projects.

I will continue next time.

Categories: Networking | Comments (0) | PermalinkEgo and Trading Do Not Mix

Posted by Mark on November 22, 2017 at 07:10 | Last modified: August 24, 2017 12:21I do not believe ego has any place in trading or in trading-related discussion.

It occurred to me that I may sound overly confident and opinionated at times when talking about financial topics. I could talk passionately when discussing many topics covered in this blog, for example. These would include option fundamentals, tenets of trading system development, financial chicanery and fraud, etc. Conviction, in general, can probably be mistaken for ego even though it may only be the manifestation of passion.

I hope I never sound too proud of my track record because past performance is no guarantee of future returns. Bill Miller epitomizes this lesson. While at the helm of Legg Mason (LM) Value Trust, Miller is credited with beating the S&P 500 every year from 1991 through 2005. For this longevity, Miller was a legend—and then the wheels came off. Miller led the smaller LM Opportunity Trust to big losses from 2007 through 2011 with a $10,000 initial investment shrinking to $4,815 (vs. $8,565 for an identical S&P 500 investment). Miller went on to trounce the benchmark in 2012 and 2013 before underperforming in 2014, 2015, and the first half of 2016 [after which he was no longer retained by LM].

Remembering that it can happen to Bill Miller should be motivation for me to maintain a large dose of humility at all times. Miller teaches us that a brilliant record yesterday does not justify inflated ego today. I feel strongly that historical trading volume and historical performance don’t make a damn bit of difference because tomorrow can be altogether different. And yes: I would pound the table passionately in support of this argument.

A corollary to this is that historical performance should not be a criterion for someone looking to hire an investment adviser.

I disagree with said corollary and that puts me in a catch-22 situation. Some have told me that promoting a strong track record is the most critical requirement for raising assets. This brings me full-circle to posts such as this, this, this, and this.

I guess it all comes down to modesty and gratitude: two things I think traders should never be without. I truly believe that how good I am as a trader will only be revealed after I click the “place order” button for the final time. Representing as if I know the answer to this any sooner through ego symptoms like arrogance or condescension would be deception at its finest.

Categories: Trader Ego | Comments (0) | PermalinkMy Take on Asset Managers

Posted by Mark on November 21, 2017 at 06:38 | Last modified: July 12, 2021 08:16Today I want to discuss my dynamic attitude toward the asset management industry.

I consider the following terms to be synonymous: asset managers, wealth managers, and investment advisers.

Throughout the course of this blog, I have not been so kind toward the asset management industry. Examples of posts where I have expressed a negative bias are here, here, and here.

I was a big more neutral toward asset managers here.

I was more positive and understanding when I decided to challenge my previous claim that the financial industry has brainwashed America.

After some further deliberation, I reached some logical conclusions here.

The asset management industry is far from perfect. Some advisers are shady and others are fraudulent. Some advisers incorrectly assert that options are too risky for retail investors while others are ignorant about derivatives altogether. Although this may represent a breach of fiduciary duty, an alternative perspective is warranted.

Without the services of asset managers, many people would basically be storing their money under a mattress. Interest rates were close to zero for nearly a decade while the average annual stock return is upwards of 11% (S&P 500 since 1926). If not for wealth managers, stocks would be an inaccessible vehicle because so many are clueless about how to do it.

I probably have two paths if I choose to bypass the asset management industry: trade for myself or bed mattress [crawl space]. One need not be a genius to be a self-directed trader but I have discussed some prerequisites. Also, as CJ suggested with the analogy of brushing teeth, the average worker may lack the flexibility to do this altogether.

Asset managers may be flawed but in the end I believe they are necessary. Regardless of their ignorance about derivatives, their consequent lower performance, and their expensive fee structure (debatable), the difference between mattress and stocks is significant. Net-net, they have a wide margin for error beyond which they can still provide a valuable service and achieve their advertised goals.

Categories: Financial Literacy | Comments (0) | Permalink