Posted by Mark on August 28, 2018 at 06:38 | Last modified: January 26, 2018 12:57

As my second TPAM to investigate, I began discussion of Envestnet before really scrutinizing their offerings. I now suspect them to be just another garden-variety, plain-vanilla IA that probably generates subpar returns and significant improvement.

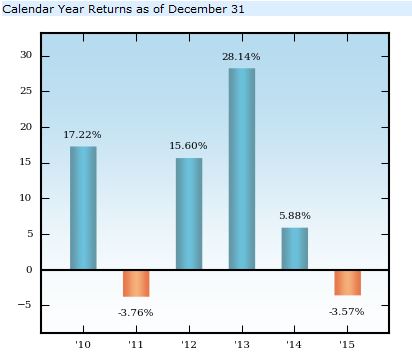

Even though the website content is “for investment professionals only” (a topic I thoroughly covered beginning here), after a bit of digging I was able to find a performance chart to assess my suspicion. Because the website appeared current when I looked at it in November 2017, I was somewhat perplexed as to why 2016 was not included. In any case:

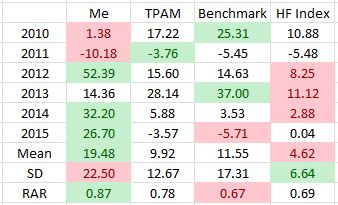

For comparison:

Green (red) shading is the best (worst) for each row. Risk-adjusted return (RAR) is average annual return divided by standard deviation (SD). Benchmark is a broad-based equity index. Hedge fund (HF) index is provided by Barclay Hedge.

My RAR beat Benchmark by 0.20, which makes me think that I performed well. I did realize a higher volatility of returns but this can sometimes be worthwhile if justified by net return. Consider that a 25% smaller position size would have lowered SD below Benchmark while still realizing a 3% better annualized return. This is why I calculate RAR.

The TPAM fared better (RAR) than Benchmark but worse than me. Cutting my position size by 45% would have lowered SD below the TPAM while still realizing a better annualized return by 0.79%. I find that surprisingly close. To look at RAR and say “0.87 vs. 0.78 is a 10% performance improvement” is misleading.*

As another angle of comparison, remember XC’s claim of outperformance by 25-50 basis points. My response was that any self-directed trader should aim to outperform by more than that. 79 is not much better than 50. I would rather see at least 150 to justify a management fee at least 1% higher. Of course, as discussed here, even a tiny management fee of 0.11% could make sense for me given ample assets to manage and no additional overhead.

Contrary to my initial suspicion, I do not think Envestnet’s showing is subpar nor, therefore, garden-variety either. It would seem that I have to be impressed with them. As another way of describing RAR [normalized for SD],* they outperformed the index by 136 basis points. Now that’s what I’m talking about! Kudos to Envestnet.

So far in my exploration of TPAMs, I have seen one good, one bad, and two that provide significant improvement.

I will continue to do more performance research to determine whether my numbers are in the ballpark of what financial institutions might be looking for in a TPAM.

With regard to my own performance, the above table has more to offer. I will discuss that next time.

* I need to re-evaluate this performance metric, which has been a favorite of mine. It might come down

to a comparison of percent difference, which is a multiplicative measure, and the additive difference of

annual outperformance.

Categories: Money Management | | Permalink

Posted by Mark on August 23, 2018 at 07:14 | Last modified: January 25, 2018 11:07

Today I conclude discussion about why some investment advisers like First Ascent and Envestnet will not speak directly to the retail clients they ultimately serve.

Picking up where I left off, I responded to Sean Gillian of Longs Peak Advisory Services:

> Would CCO [Chief Compliance Officer] apprehension about

> performance reporting, which may lead to problems with the

> SEC if not done properly, be mitigated if IAs were willing to

> undertake the expense of becoming GIPS complaint and verified?

Gilligan responded:

> Some CCOs don’t want to be GIPS compliant… [and verified]…

> because they consider that a risk. False claims of compliance

> are a risk so they worry about taking on the additional

> burden of making sure they are complying with something they

> are not otherwise required to do. In reality the SEC likes

> GIPS, but they do take the claim very seriously to make sure

> you truly are compliant if you say you are.

I am reminded of a financial advisor perspective suggesting greater liability for publishing inferential statistics where I wrote:

> Advisers should not publish statistical analysis because they

> may overstate importance to the uneducated reader? In my

> opinion, statistical analysis is necessary to suggest a

> difference might be meaningful. And only the author can do

> the statistical analysis since the entire data set is rarely

> (if ever) presented in the article itself.

Backing claims with statistics is the right thing to do because empty claims are potentially contaminated with underlying motives of sales and marketing teams. Similarly, I believe [GIPS compliant and verified] performance reporting is the right thing to do for anyone investing money for others. In both cases, doing the right thing seems to be the risky alternative.

Are regulations to blame for this non sequitur? I asked Gilligan:

> Is it a matter of their compliance department (or firm) not

> having a full understanding of the regulations, which makes

> them recommend erring on the side of caution?

He said:

> It is… compliance wanting to keep their job simple.

I asked:

> Why are portfolio managers [PM] okay with this? Do they

> realize compliance directs them to operate in this way out

> of a desire to “keep their job simple?”

Gilligan responded:

> I wouldn’t say that PMs are okay with this. Many firms have

> an ongoing debate between PMs/Marketing and their compliance

> department regarding… [advertisement of performance]. Larger

> firms form working groups with representatives from both sides

> that work to determine a compromise that everyone can live

> with and that becomes their firm policy.

>

> I agree with you that GIPS compliance is best practice and

> there should be transparency, but unfortunately it gets more

> complicated when compliance people are overly scared of

> regulators finding deficiencies in what they do.

He also pointed out that GIPS compliance is separate from general regulatory compliance (e.g. SEC or state registration), which makes me wonder what compliance members get scared. I would not think a firm like Longs Peak gets scared of regulators finding deficiencies. Longs Peak has experience and specializes in GIPS compliance. If they have doubts about whether they can do their job properly then I certainly would not want to hire them!

Unanswered questions remain but compliance and regulations seem to be complicating matters about the right thing to do.

Categories: Money Management | | Permalink

Posted by Mark on August 20, 2018 at 06:59 | Last modified: January 25, 2018 10:54

First Ascent’s reason for not speaking to me directly made sense but I did not remember any such SEC requirement from my Series 65 study. Since I am trying to learn about the industry, I e-mailed Sean Gilligan of Longs Peak Advisory Services.

Gilligan wrote:

> The SEC does not require performance to be presented in a

> 1-on-1 setting, but they do deem anything… presented outside…

> a 1-on-1… to be an advertisement. Advertisements are subject to

> more rules and disclosures than what is required when meeting

> 1-on-1 for a customized presentation.

>

> Likely the performance they have available to show is model

> performance… [always highly scrutinized by the SEC] rather

> than a composite of all actual accounts, which is what GIPS

> would require… it is easier for them to have you sit down

> with an advisor… [who] can… explain… differences that…

> exist between… model and a live account than… to make a

> broadly distributed advertisement piece…

Sounds like a legal proceeding with attorney dictating what can or can’t be answered, how to phrase responses, etc.!

I replied:

> As an IA, I would want to publish performance without need for

> a 1-on-1 consult. Being GIPS compliant, would I be able to do

> this? What really frustrates me is the fact that if I were to

> hire an advisor who sold funds from this company, I could not

> directly speak with those executing discretion over my money.

I am not able to speak with traders at a mutual fund but I can call and speak directly with a fund representative!

Gilligan responded:

> To clarify, you can show performance outside a 1-on-1 as

> long as you have the right disclosures and have calculated

> performance in an acceptable manner (e.g. SEC requires

> broadly-distributed performance to be net-of-fees, while

> 1-on-1’s can be gross-of-fees). As a GIPS compliant firm you

> would be REQUIRED to distribute performance to all prospective

> clients… [this firm] you spoke with probably had an internal

> policy not to distribute performance. Many CCOs are very

> conservative… [on this] because they feel it is too high

> risk… [may lead to SEC issues if done improperly]. Most

> likely the firm’s CCO made a policy not to distribute and

> blamed it on the SEC when explaining… Truly they could if…

> they… [took] the time to include… necessary disclosures.

I don’t blame First Ascent for bending the truth. Simplified explanations are best for laypeople.

I will conclude next time.

Categories: Money Management | | Permalink

Posted by Mark on August 17, 2018 at 07:29 | Last modified: January 24, 2018 06:35

I want to be able to communicate with the entity responsible for investing my money. Like First Ascent, though, the Envestnet website says “for investment professionals only.” It is not intended for private investors. Private investors interested in their investment services are told to contact a financial professional.

I asked First Ascent about this and got the following response:

> We aren’t able to provide performance directly to clients

> without an advisor. Because we do not work directly with

> retail clients, and offer our strategies only through FAs, an

> advisor is required to… present gross-of-fee disclosures

> regarding advisory fees along with performance.

>

> If you are interested I’d be happy to have a call and answer

> any other questions that you have.

I prodded further and asked why they would not discuss performance with me directly.

> I apologize that we can’t provide performance directly. The

> reason is that the SEC requires performance be presented in

> a one-one-one conversation by an IA who can provide

> prospectuses of funds used and information regarding the

> structure and fees of the underlying ETFs and mutual funds.

>

> Our strategies may also vary in their underlying holdings

> based on the requirements or preferences of the advisors we

> work with, and some strategies are restricted to advisors from

> specific organizations, so performance may vary.

See my comments on separately managed accounts.

> Because of this we prefer to distribute performance directly

> through the advisors we work with who can provide these

> disclosures and make sure they are providing performance

> for the appropriate strategies that they use.

This actually seems like a decent argument to me.

> If you are interested in working with a financial advisor I

> am happy to provide the names of some firms that utilize

> our strategies in your area.

I give them kudos for being courteous.

All of this reminds me of behind-the-counter (BTC) products at the pharmacy. BTC has been controversial since 1984 when a proposal was filed to change ibuprofen from prescription to over-the-counter (OTC) status. Opponents argued the switch could cause patient harm. Instead of being granted OTC status, many suggested the drug be placed in a new class of medications to be sold only in pharmacies despite not requiring a prescription for purchase.

Proponents of BTC argued that pharmacist counseling would add a layer of safety.

BTC opponents included the pharmaceutical industry and clinical physicians. The former claimed pharmacist counseling would not benefit the consumer. The latter argued counseling and gatekeeping BTC drugs were tantamount to practicing clinical medicine, which pharmacists are not properly trained to do.

In the same way that I believe pharmacists can provide necessary education and enhance public safety by dispensing BTC products (e.g. insulin, Sudafed), I also believe it makes sense to have a financial [literate] professional [without underlying motives] present performance information to put it in the proper perspective.

I will continue next time.

Categories: Money Management | | Permalink

Posted by Mark on July 31, 2018 at 07:40 | Last modified: January 17, 2018 07:59

Today I conclude analysis of an e-mail from Todd Tressider of www.financialmentor.com. My belief that the financial industry offers less genius and innovation than its marketing and advertising portrays ties back to why we need not bestow fiscal responsibility on those who have previously violated public trust.

> For most people wealth is not the result of learning the latest

> investment technique at an over-priced weekend seminar, discovering

> unknown secrets, or pursuing other magic pill formulas.

I think this is a great point. The secret sauce pitch sure is alluring: see it for what it is.

> As John Bogle correctly stated, “The secret is there are no secrets.”

Great quote! I previously discussed proprietary offerings and I still have more to say on that in a future post.

> That’s why designing your personalized wealth plan is the make-or-

> break starting point. Get this step wrong and much future effort is

I somewhat agree with this. Financial advisers often advertise design of a wealth management (WM) plan tailored uniquely for the client. I don’t believe such plans need be as unique as they claim.

> misplaced and generally wasted. Get it right and your financial goal

I won’t disagree with that…

> is virtually assured (as long as you persist with sufficient action).

>

> It’s literally that simple.

… but I will disagree with this. Nothing is guaranteed—perhaps not even “virtually”—when it comes to making money. Very few things are “simple,” either: especially hard work.

> The truth is wealth doesn’t require genius, special talents,

> privilege, or luck. Those are all myths.

I agree! I think time-tested approaches can take us a long way.

> It also doesn’t require any more work than financial mediocrity. It

> is not about working harder: it’s about working smarter…

I somewhat disagree with this. I think people who claim to work “smarter” are gifted with intelligence (unnecessary here as just mentioned), developed with regard to cognitive strategies, or making excuses to be lazy. Those in the first two groups are successful. The latter group includes smooth talkers who I have seen fail. Hard work may take additional time but is more likely to get the job done. Taking shortcuts may amount to gambling in hopes that the essential elements will be completed.

> In addition, your plan gives you a context for judging all the

> “bright-shiny-objects” that can distract you. You’ll know what

> fits, what doesn’t, and why.

Great point! See the second prerequisite discussed here.

The promise of unique fit and custom tailored is an emotional sales tactic because if you think someone cares enough to understand your particular situation then you are more likely to trust (establishment of rapport). This tactic can also serve as a distraction from a shady professional history, which is much more important than particularly individual.

See through the veneer because I seriously doubt a unique wealth plan is necessary for everyone. According to Genome News Network, people are 99.9% identical with regard to DNA. The influence of ego makes us feel particularly individual in our own minds. In reality, though, we’re all human beings who can be broken down into a few different categories when it comes to risk tolerance, financial goals, and WM.

Because it’s no more complicated than that, promising something exclusive is really not necessary.

And as Tressider said above, genius (or innovation) is also unnecessary for an effective WM plan. That “proprietary” label establishes an aura of mystery and intrigue when time-tested approaches will do just fine. Once again, do not be distracted from more important details such as the quality of person with whom you are dealing. While I generally believe in giving people second chances, avoid people or entities with a history of chicanery when it comes to your hard-earned money.

Categories: optionScam.com | | Permalink

Posted by Mark on July 26, 2018 at 07:13 | Last modified: January 17, 2018 07:14

Today I will dissect a recent e-mail received from Todd Tressider of www.financialmentor.com. This message is a preamble to a series of e-mails on designing a wealth plan. Tressider describes himself as a “money coach” and offers many resources at his website. My critical analysis subsystems are activated because while I cannot vouch for his quality of information, I can easily identify his premium offerings for sale.

> How do postal workers and teachers achieve financial security while

> certain doctors and lawyers get stuck in financial mediocrity?

More appropriately, certain postal workers and teachers because the odds are against them for purposes of this comparison.

> Why do some people work hard and end up broke while others exert

> far less effort and make millions?

I think he’s picking at the extremes here. I will venture to say most people who work hard have something to show for it; most people who do nothing have very little.

> Answer: the winners have a plan based on proven principles…

“Proven” is a hollow claim. Conventional wisdom exists, which sometimes leads us astray. Attributions of success are anecdotal and “he said, she said.”

> I know it sounds too simple and probably a little boring, but it’s

> the only thing that works consistently in practice. Believe me…

> I’ve tried ’em all…

I don’t believe him. I can easily imagine someone not trying everything without even realizing it.

> …If you want wealth in this lifetime with a high degree of certainty

Based on what sample size does he claim a “high degree of certainty?” Without supporting evidence, I doubt this is a valid categorization. Remember my recommendation to challenge everything when someone has something to sell.

> then there is no substitute for designing a plan where you set goals,

> take consistent action, and practice daily habits that lead to wealth.

I agree because I consider much of this a subset of “hard work.”

> Your wealth plan is a powerful tool because it creates clarity,

> congruency, and consistency in your actions so you know exactly

> what tasks to accomplish each day, week, and month to reach your

> goal. No confusion or complication…

Nice alliteration here. Aside from that, I do agree that checklists can be very useful. Michael Mauboussin discussed this in The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing (2012).

> We are all given the same 24 hours in a day but we won’t all

> achieve our financial goals… your wealth plan is essential.

> Without it your goals are a rudderless ship spinning in

> circles with no clear direction. Your results are random.

Tressider has some good stuff here.

I will conclude next time.

Categories: optionScam.com | | Permalink

Posted by Mark on July 23, 2018 at 07:02 | Last modified: January 15, 2018 12:12

“GetFolio.com” offered a guarantee in our last installment, which served as a springboard for my skepticism.

If in doubt then do your internet research. I found a forum post by “Ray” about the web site in question:

> I would offer a guarantee like that if I was selling a service in

> which I had no confidence. Following bad advice for a year to try

> to get a $600 refund is a bad idea. To qualify for the guarantee, I

> cannot tell if you must buy all of the “timely recommendations” or

> just buy only from that group. Also, when do you close a position?

>

> The [site lacks] concrete info… an annual performance table for

> the last 16 years (live for the last 10) has no other numbers like

> intrayear drawdown. They calculate performance using stock price

> when first suggested and year-end price. I don’t know how they

> handle stocks sold during the year or held past year-end. I did

> not see much info about exits on the site…

>

> [I can’t] see what they actually do without buying a subscription…

>

> No model portfolio or any other way to verify their performance is

> available. They appear to suggest too many stocks to actually buy.

>

> I might like this service, but there are just too many loose ends.

If it seems questionable to you then it probably is to others as well. I highly recommend making use of the knowledge-sharing platform that is the Internet.

A post from another forum answers some of Ray’s questions:

> I wanted to comment on my one year subscription ($600) with this

> lousy company. First, their philosophy is to invest in very small

> amounts–equal to 1/4 of 1% of the total amount you have to invest

> per stock recommendation. Second, they only give you recommendations

> when the market tanks… To become fully invested… would literally

> take several years. After you calculate service cost and cost of

> stock transactions, you would likely be losing money the first few

> years until significantly invested… My problem isn’t necessarily

> with their philosophy as it is their guarantee… if you don’t beat

> the market, they will return your money. But you have to subscribe

> the whole year and provide proof of recommended stock purchases.

> In my case, not only did they not beat the market, I didn’t receive

> any recommendations! Not one! According to tutorials, you’re not

> supposed to purchase when the “Market Gauge” is > 20… [which meant]

> I didn’t receive any recommendations for the whole year. Their

> response? “The guarantee is only for new subscribers who follow

> the recommendations and can provide proof.” How’s that for customer

> service? “Hey, sorry we didn’t provide you with any recommendations

> but I’m sure your $600 taught you something!” Yes… buyer beware!

Is this just a shill from a competing service? He doesn’t write with excessive gloss. He gives lots of consistent details. He makes sense. I personally think he’s conveying actual personal experience.

As with anything, you ultimately have to decide for yourself what reviews you believe. The more you read, the more of an appreciation you will get for different styles ranging from blatant deception to honest reality. I deem this to be the latter, which makes me reflect upon my skepticism and think “I couldn’t have said it any better myself!”

Categories: optionScam.com | | Permalink

Posted by Mark on July 20, 2018 at 06:30 | Last modified: January 15, 2018 11:20

As a PSA on the existence of shady tactics in the financial industry, I have been dissecting credentials originally tied to a bogus article/advertisement on riskless collars. Today I continue the journey by analyzing content from GetFolio.com.

> Two things GetFolio.com does better than anyone else, and I

> guarantee it…

Guarantees of performance are prohibited by the SEC. For that reason, the mere presence of the g-word in any promotional material for financially-related products is a red flag to me. Unless pertaining to a bond,* the word “guarantee” is not necessary and does not belong in financial marketing. Ever.

> Ask yourself a simple question: Is investing a hobby, or is it a

> serious business that you believe can make you real money? If it’s

> a serious business, then what is it worth to ensure that you don’t

> waste thousands of dollars, struggling to get ahead with risky and

> ineffective techniques?

If it’s a serious business then you will be relying on yourself to learn/develop strategy as opposed to potential shysters selling trade ideas. I wrote about this here.

> Try it now!

> It really works

Any verbiage that seems too cheesy, aggressive, superficial, or pushy is a red flag. I believe people with true investing skill are humble, respectful, and will let the numbers (if there are any) speak for themselves.

Another theme I have seen in the newsletter/advisory industry is a tendency for charlatans to step on the backs of crooks. In navigating to the “guarantee” tab:

> A healthy dose of skepticism about web-based businesses, much less

> those that provide investment strategies, is a good idea…

Encouraging skepticism—even about a category [web-based businesses] to which he belongs—makes him appear more credible. Several times I have read/heard such content from people later named in SEC Complaints.

While believing myself to be authentic, I have encouraged skepticism many times in the blog so I do not consider it a deal breaker. I am also not selling anything here. If I were then I might avoid these optionScam.com posts altogether. I simply want to acknowledge the presence of hypocrisy in the financial industry along with the fact that recommending skepticism for personal protection is sometimes a sales tactic. Don’t forget to apply that scrutiny to whoever/whatever is offering the advice.

> The GetFolio.com performance guarantee is offered to new

> subscribers only… To qualify for the guarantee, you must

> maintain a log of all trades taken throughout your subscription

> period, documented via legitimate proofs of purchases.

That seems too loose for me. Do I need to hold positions until the service finally recommends closing at huge losses? How much money could I lose across all positions before seeking refund for a few hundred bucks? Would I be willing to send actual brokerage statements to a stranger to get my money back? Aside from security issues, the time and effort required to collate all this might not be worthwhile.

I will continue next time.

* A non-cancellable indemnity bond whose principal and interest payments are backed by an insurer is “guaranteed.”

Categories: optionScam.com | | Permalink

Posted by Mark on July 17, 2018 at 06:50 | Last modified: January 14, 2018 09:14

As part of my annual discussion on fraud, today I continue my analysis of ChangeWave Investing.

I next started to research Jon Najarian, a character I’ve seen, heard, and read many times online over the last 10+ years:

> Jon Najarian is the founder of InsideOptions.com, and editor of

> ChangeWave Options Trader (ChangeWave.com)…

Being linked with an entity linked with a fraud is enough to get me to run the other way. As I said last time, I generally think people deserve second chances but not when it comes to my hard-earned money. I strongly advise you adopt the same outlook. Let these people get their second chances with jobs carrying less fiscal responsibility.

> About ChangeWave Options Trader

>

> ChangeWave Options Trader is a weekly advisory newsletter service…

> Jon Najarian and the ChangeWave Research Alliance’s goal is to deliver:

>

> Trades that are successful 75%-80% of the time…

> Winners that deliver 65%-75% gains as a regular course…

If it sounds too good (e.g. consistent 65%-75% gains) to be true then it probably is.

> A few 200%-300% winners

Claims of extremely outsized performance are red flags. Most aren’t real.

> ChangeWave Options Trader helps subscribers multiply profits as much

> as tenfold, making one to two trades each week, and at the same time

“Multiply profits as much as tenfold” is a claim of outsized performance. Don’t believe it.

> slash the risk factor with their “Pro’s Edge” trading strategy. They

Proprietary names of services/features that sound technically advanced or secretive are red flags. On many occasions, I have found little actual content behind these titles.

> help subscribers avoid mistakes that trap most amateur options

> investors, by using options the way that pros do.

Out of curiosity, I then poked around to learn more about this website I had stumbled upon:

> The “wonderful” results of most systems are often the result of

> computer modeling and the ability to pick the best curve to make

> the retrospective data appear the most positive. When followed

> prospectively, many of these models perform much more poorly.

I completely agree! I was intrigued.

> What makes GetFolio different?

Claims of being different (or unique) are potential red flags characteristic of many sales pitches. By this point in history, I don’t think much in the way of genius or innovation exists with regard to successful investing. Commitment, above all else, is what’s required and what so often seems to be missing.

> The GetFolio.com system was developed and tested, using real

> money on thousands of stocks in both bear and bull markets…

I’m leery of that claim. I doubt they could substantiate real money trades on thousands of stocks in different market environments. That would require quite a bit of capital and an impressive feat of documentation.

I will continue next time.

Categories: optionScam.com | | Permalink

Posted by Mark on July 12, 2018 at 07:18 | Last modified: January 12, 2018 04:53

Dissecting and exposing Changewave’s “riskless collar” returns me to the path of public service announcements (e.g. here and here). I want to remind you that suspicion can never be relaxed about the financial industry notorious for bad apples.

I often do internet research because a wealth of information lies in wait to be found. I looked for reviews of Changewave Investing. Online reviews are dicey because they may or may not be sincere. Positive reviews are sometimes shills for the company (including friends, family, and marketing partners). Negative reviews may be industry competitors. The more I read, however, the more I feel I’m able to separate wheat from the chaff. The overall gist may offer some meaningful nuggets and red flags. To some extent, I go with my gut.

I found “Tobin Smith” linked to ChangeWave, which led me to this worthwhile article. Roughly halfway through I found:

> Likewise, in March, the SEC settled a fraud case with Tobin Smith

> of the NBT Group, a publication service also known as “Next Big

> Thing Investor” and formerly named ChangeWave. The SEC

> alleged that he failed to fully disclose how much he was being paid

> to promote the stock of IceWEB, a fledgling data-storage company.

> The problem here, for the SEC, was that he didn’t disclose he got

> additional incentive pay if the stock went up. Smith and NBT neither

> admitted nor denied the allegations in the settlement, but he has

> to cough up profits and pay a fine [emphasis mine].

Anyone in the financial domain who has ever been linked to fraudulent activity should be avoided. This is an exception to my general belief that people deserve second chances. Too many times I have seen hucksters get “slaps on the wrist” for their misdeeds, which leaves the door wide open to recidivism. Take no chances with your hard-earned money; avoid those with a history of deceit.

After questioning Changewave before, I was now even more convinced about their illegitimacy.

As an aside, this article reminds us to be very leery of “hot” stock tips found online:

> The problem is, all of this was a lie to dupe investors, the SEC alleges

> in a complaint filed against Peterson in March. Peterson made the

> bogus claims in the company filings, and backed them up with posts

> on an InvestorsHub.com chat board during 2012-2013, says the SEC.

>

> Using the pseudonym “dick_schmidt,” Peterson posted over a hundred

> times to the RV Plus board, calling the company “undervalued” and

> urging investors to “buy up as much as possible…” When other

> posters question his company’s financials, he responded: “Fed filings

> don’t lie.” He also posted that if the contracts were bogus, someone

> “would have detained the CEO or whoever was responsible for faking

> something this extreme. Let’s use our common sense here…”

>

> …Don’t trust message boards unless you know who is really posting.

Great advice!

I will continue next time.

Categories: optionScam.com | | Permalink