When Performance is Irrelevant (Part 3)

Posted by Mark on April 24, 2017 at 07:32 | Last modified: November 22, 2016 09:48In this blog mini-series I’m considering the possibility that financial performance reporting is at least misleading and at most irrelevant. As a third example, today I will discuss a prospectus for the T. Rowe Price Value fund.

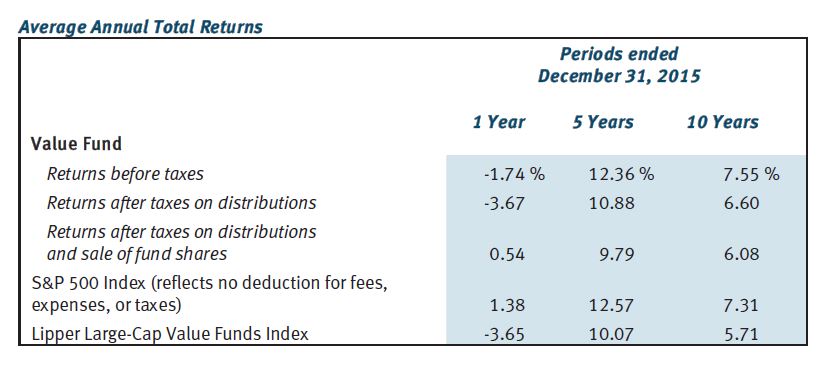

First, take a look at the following table:

This gives us something against which to compare the fund’s performance. The Value Fund outpaced S&P 500 over 10 years but fell short over one and five. Value Fund beat the benchmark (Lipper Large-Cap Value Funds Index) over all three time frames but operating expenses (0.81%) are not included. Your actual performance would therefore fall short of the numbers reported here.

Once again, why be deceptive? Why not provide a historically accurate report of how the fund performed?

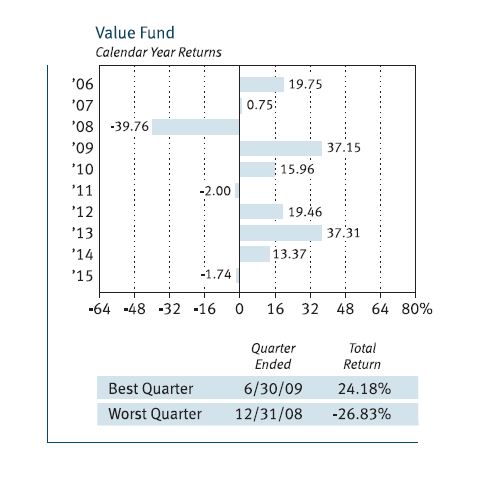

The prospectus also includes the following graph:

This gives us a 10-year track record to look at, which is better than the two years seen with American Funds Growth Portfolio. Ten is still a small sample size, though.

What may be worse is that each of the 10 samples is itself far too small a sample. I mentioned this with regard to the Vanguard prospectus: we do not see any error bars on the graph.

What happens in any particular calendar year is only one representation of an infinite number of potential occurrences. What if a large bankruptcy had been announced December 29 instead of January 5? What if Friday fell on the 31st instead of the 1st causing a jobs report to be delayed a week? What if a verbal misunderstanding, a dropped call, or a random muscle twitch had resulted in two countries going to war?

The fact that altered events can theoretically result in significant performance differences suggests just how trivial any single sample is. For me this is strong motivation for Monte Carlo simulation.

Monte Carlo simulation is a methodology used to generate large sample sizes. Given a system with many trades, toss the profit/loss numbers into a hat, mix thoroughly, and pick randomly to get different trade sequences. This can be done thousands of times. Robust descriptive statistics may then be used to generate and discuss probability-based future predictions of performance.

Monte Carlo simulation is unfortunately the exception—not the rule. Singular performance numbers based only on specific historical records are routinely reported. Laypeople in droves (along with their investment advisers) make frequent decisions based on these reports that, I would argue, are statistically meaningless.

This is a big reason why I suspect financial performance may be irrelevant.

Categories: Financial Literacy | Comments (0) | PermalinkWhen Performance is Irrelevant (Part 2)

Posted by Mark on April 21, 2017 at 06:19 | Last modified: November 18, 2016 10:26In this blog mini-series I’m considering the possibility that financial performance reporting is at least misleading and at most irrelevant.

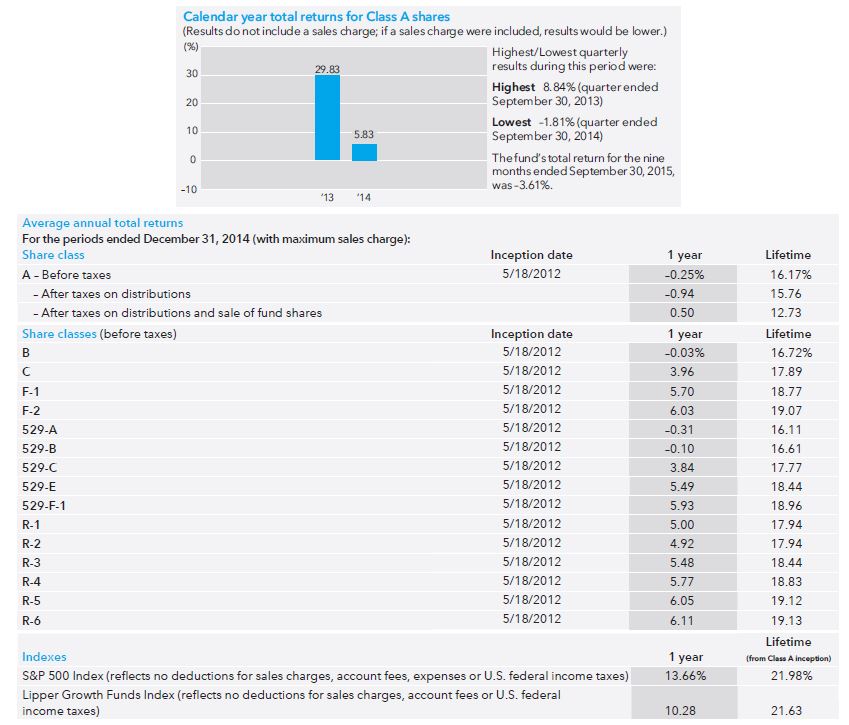

Last time I briefly discussed a prospectus for a Vanguard fund. As a second example, let’s look at the American Funds Growth Portfolio prospectus:

The first thing I noticed here is the short track record. The bar graph only shows performance for two years since the fund opened May 2012. Instead of 10 tiny samples (Vanguard), here we have two tiny samples.

An additional problem is a failure to include the sales charge. The disclaimer “if a sales charge were included, results would be lower” is nice but they don’t tell us how much lower it might be. I would like to see the maximum possible sales charge included as they did in the table. If the worst-case performance is acceptable then I’m more likely to invest. Either way, the point of a graph is to show and they failed to do that because what they graphed is not realistic.

The table indicates that every share class (of which there are many) underperformed the S&P 500 and the benchmark (Lipper Growth Funds Index). This is not encouraging but again, the sample size is sufficiently small here to mean very little. For a quick second I am happy that they at least included the sales charge.

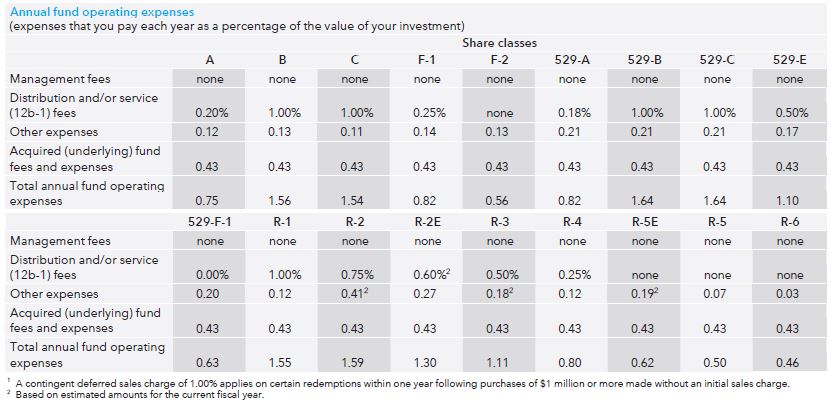

But don’t think for more than a second that they reported the actual performance because other fees are not included. Evidently it does not pay to look only at the performance section because earlier in the prospectus we see:

“Operating expenses” range from 0.46% – 1.64% annually. I called to get more information and only Class A and Class C shares are available to me as a prospective retail investor (“individual nonqualified account”). That means I would be stuck with a 0.75% annual fee on top of a 5.75% load (sales charge) and 1% redemption charge or a 1.54% annual fee with no load and a 1% redemption charge. Unfortunately neither annual fee nor redemption charge is included in the graphs or the tables, which means the reported performance numbers are optimistic exaggeration.

Is this deceptive advertising?

I will continue next time with one final example.

Categories: Financial Literacy | Comments (1) | PermalinkWhen Performance is Irrelevant (Part 1)

Posted by Mark on April 18, 2017 at 07:26 | Last modified: November 18, 2016 12:45Plenty of reasonable doubt suggests traditional reporting of financial performance is irrelevant and serves only to mislead.

I am not saying reporters of financial performance are aiming to mislead. This post is not categorized optionScam.com. Reporters may occasionally attempt to mislead but certainly not always. I also believe financial reporters often mean well and do exactly what their compliance teams require (e.g. for mutual funds or hedge funds). This can still fall short of the mark, however, which is why society as a whole needs increased levels of financial literacy.

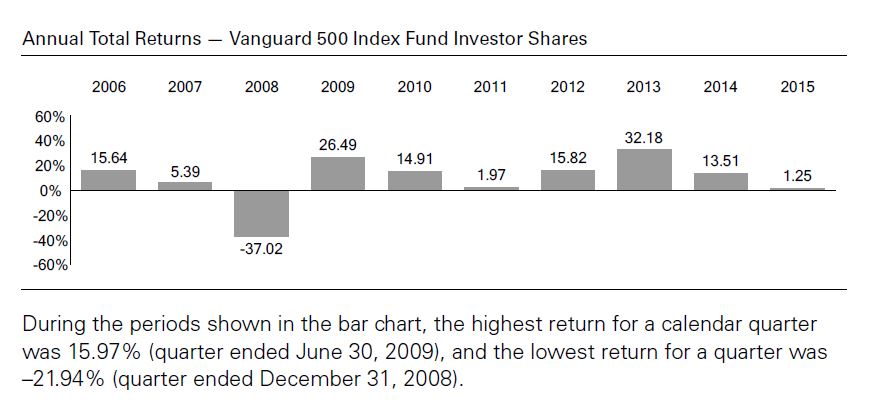

I begin by taking a look at how investment performance is presented today. I did a search for “mutual fund prospectus” and took three hits from Google page 1. Let’s start with the Vanguard 500 Index Fund:

The main critique I have of these numbers is that each year includes only one sample. We don’t see any [standard] error [of the mean] bars here: each number is exactly what the fund returned during that calendar year. People tend to give samples created from a linear combination of historical data added weight and sometimes these historical samples (as opposed to simulated trials) are the only ones people recognize. Statistically speaking it is one and only one sample, however, which makes it the tiniest sample size available aside from zero. I had the same criticism for Craig Israelsen.

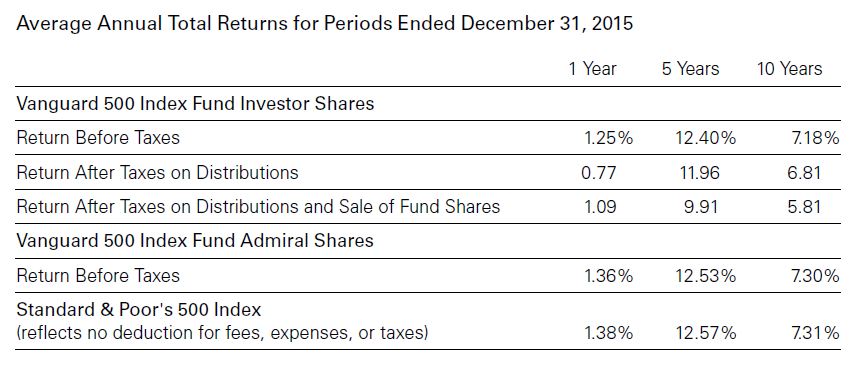

The prospectus also includes the following table:

Nowhere does it state that transaction fees are included in the performance numbers. Transaction fees are mentioned in the last row where benchmark performance is given. While this may imply the fees are taken into account above, we cannot assume this.

I will make one tangential observation here about relative performance. The fund underperforms the benchmark for all three time frames whether looking at Investor Shares or Admiral Shares. Critics of actively managed funds sometimes emphasize large losing margins against the benchmarks. The only way to ever beat the benchmark is to actively invest. A passively managed fund is guaranteed to lose every time because of the fees—regardless of how small those fees might be.

I will continue with two more examples in the next post.

Categories: Financial Literacy | Comments (3) | PermalinkCost of Doing Business (Part 2)

Posted by Mark on January 30, 2017 at 07:31 | Last modified: November 23, 2016 11:19I believe clients pay millions of dollars every year to have money invested less effectively than they could do themselves. Rather than seeing this as financial-industry brainwashing, however, it may be a simple cost of doing business.

Two necessary components must be in place if the financial industry has indeed perpetrated a brainwashing of the American public. Even if the vast majority of people believe in domain-specific expertise, “brainwashing” implies a widespread propaganda campaign run by the financial industry. I’ve had some casual conversations with investment advisers and I read financial journals regularly. The brainwashing assertion seems too far-fetched for me to accept.

Here is a more positive perspective: investment advisers work as intermediaries. If I am going to pay someone else to replace my brakes then I will pay more to have it done. Similarly, if I am going to hire an adviser or fund operator (by purchasing shares) to invest my money then I will pay more to have it done. The added cost comes in the form of management fees, operating expenses, and lower returns as a result of less-efficient strategies.

Neither financial professionals nor the financial industry are to blame in this new paradigm. The industry is doing what clients ask them to do: invest money. Compared to the alternative—leaving money in savings accounts or under the mattress where inflation-adjusted returns are negative—the industry is doing a good job. Financial professionals may not match the performance of self-directed investors but time is required to learn and to do it for oneself. What you gain from being self-directed is partially offset by the time and effort committed.

In the new paradigm, this is about sweat equity. Those skilled at the trades (e.g. carpentry, plumbing, electrical) are in a good position to invest in real estate because they can fix things cheaper and realize a lower cost basis on property. Those with a penchant or aptitude for math and finance can invest/trade and realize a lower cost basis as well. Those who don’t must leave it to the professionals. In doing so they will pay a premium to have done what they can’t do themselves.

And they will be willing to pay the premium because that is how our capitalistic society works. It doesn’t have to be about manipulative brainwashing; it can simply be about appreciation and gratitude for a service.

Categories: Financial Literacy | Comments (3) | PermalinkCost of Doing Business (Part 1)

Posted by Mark on January 27, 2017 at 06:07 | Last modified: November 23, 2016 08:59Long-time readers may not be surprised to hear that I am sometimes jaded and skeptical of the financial industry (e.g. optionScam.com). Seen differently, however, perhaps this is just the cost of doing business.

According to some of my teachers/mentors over the years, the financial industry has brainwashed the public at large. People believe investing is an important, responsible enterprise that is best left to the [financial] professionals. I agree with the former and disagree with the latter. I believe many financial/investment advisers are glorified salespeople who push products their firms are contracted to sell. I discussed this in detail here.

Along these lines of thinking, the financial industry has brainwashed society to pay more and expect less. A standard management fee has traditionally been 1% of assets under management per year. In exchange, savvy clients have expected to beat the benchmark.* This means when the benchmark loses money, clients should remain satisfied as long as they do not lose more. Paying someone to lose money that you could lose yourself is anathema to me.

Financial brainwashing also includes the acceptable sale of inefficient services. This involves getting clients to pay up for less-efficient investment strategies than what they could employ on their own (think long stock instead of trading options). Society seems to be comfortable with and accepting of this.

I occasionally seem so down on the financial industry! I feel like a closet conspiracy theorist and I do not like it. My preference is to be positive and encouraging about things.

The time has come to challenge the assertion that society has been brainwashed. A cursory evaluation reveals two components that must be present for this brainwashing to have taken place.

The first component would be a widespread belief that the financial industry has a proprietary edge. Truth be told, I have little understanding what the “public at large” thinks about financial matters and I doubt I’m alone on this. The issue to survey is whether investing success is a result of domain-specific expertise or simply a matter of having the right education. Domain-specific expertise might involve professional research teams able to cover a large number of companies/industries or professional stock pickers powered by innate talent and lengthy experience: forms of expertise no laypeople could develop on their own.

I will continue this discussion in my next post.

* This is changing with the promotion of passive/indexing investment strategies, which always fall a bit short.

Concannon on Stock Splits (Part 2)

Posted by Mark on December 26, 2016 at 07:26 | Last modified: October 6, 2016 16:31Chris Concannon is CEO of Bats Global Markets. Today I will conclude analysis of his article “Stock Splits for the Middle Class,” which was recently published in Modern Trader magazine.

Concannon suggests targeting “buy and hold” investors (for which he provided no evidence) is somewhat classist:

> While it’s nice for a company to say it

> wants to attract long-term buy and hold

> investors, failing to split a high-price

> stock encourages small investors to avoid

> a stock altogether or causes them to pay

> a substantial penalty when they trade

> such a security… One could argue that a

> company’s refusal to split its stock is

> a refusal to embrace middle class retail

> investors with less investable wealth.

Concannon qualifies himself nicely here by saying “one could argue.” The argument would be stronger if he could provide some evidence that higher-priced stocks are eschewed by a significant number of retail investors. Maybe it doesn’t make a meaningful difference given the dominance of institutional traders but I would at least like to see some effort to offer more than empty claims, which I consider speculative and meaningless.

Concannon closes with the following:

> When debating… the goal of making stock trade

> better, we should also focus on… stock splits.

> While this is self-serving to a degree, given

> our per-share revenue model, the evidence is

> clear that many investors would save money and

> more investors could participate.

This, along with many ideas in the article, makes logical sense. Unfortunately many logical ideas in finance do not bear fruit. I am baffled as to why he says the evidence is clear because he provided no evidence in the article. If there is clear evidence then please show us! As written these are nothing more than hollow claims.

What is clear from this final paragraph is Concannon’s agenda, which I believe helps to categorize this article. As the CEO of a major stock exchange, his corporate revenue is proportional to share volume. I consider this article a marketing piece to encourage greater use of the stock split. I also consider this an editorial since it includes no supporting evidence. A table showing number of stock splits per year seems like a no-brainer to include. I probably walk away more skeptical since such simple data is not presented.

I believe we should always read critically for the most complete understanding. Reading critically includes understanding the writer’s agenda. Writers aim to persuade, which is in their best interest. Being persuaded is not always in the best interest of the audience, however. Critical thinking is a very useful tool to defend against being persuaded by lower-quality [sometimes false] information.

Categories: Financial Literacy | Comments (0) | PermalinkConcannon on Stock Splits (Part 1)

Posted by Mark on December 23, 2016 at 06:48 | Last modified: October 6, 2016 16:01Chris Concannon is CEO of Bats Global Markets. He wrote an interesting article recently in Modern Trader magazine called “Stock Splits for the Middle Class.”

Concannon begins by presenting some data to suggest current stock trading is weak and depressed:

- Average share volume for the 12-month period ending April

30, 2016, is down ~9% from the same period four years ago - Notional volume during this period is up 15%

- Share volume in January 2016 is up 1.92% while

notional volume is up 42% compared to January 2010

Weak/depressed trading is seen by a lack of significant share-volume growth. More notional value traded on equal or lower share volume suggests stock appreciation is outpacing stock splitting. I would have liked to see how these numbers compare to other historical periods for a stronger case, though.

Concannon believes the refusal of corporations to split stocks is one limiting factor on share volume:

> In an ill-conceived effort to attract “long-term

> investors” and detract “speculators” from trading

> their stocks, a number of popular U.S. companies

> have kept their nominal stock prices above $200,

> $500 or even $1,000 per share.

This is an interesting claim but no evidence is given to support it. If he is referencing a conversation(s) or quote by directors or C-level execs then he should most assuredly cite them! The use of quotation marks implies credibility but a critical reader cannot assume these to be actual words spoken by others.

Concannon goes on to explain the psychological impact of higher stock prices. He begins:

> An average individual investor may avoid a $500

> stock as being too richly priced but change his or

> her view when that security is split 10-for-1 and

> then trades at $50 [emphasis mine].

This makes sense but the actual impact is unspecified and I’m not sure it could really be measured. Concannon qualifies the statement well.

He then goes on to suggest the wider bid/ask spread is a significant drawback when trading more expensive stocks. He argues stock splits, while leading to higher per-share commissions, would more than make up for this by improved liquidity. In theory this makes sense but it is just that: theory. Why not interview some big institutional traders to see if they agree? This would be compelling evidence. Without any evidence it remains an empty claim.

I will conclude with my next post.

Categories: Financial Literacy | Comments (1) | PermalinkPerspectives of a Financial Adviser (Part 5)

Posted by Mark on December 18, 2016 at 04:52 | Last modified: September 14, 2016 05:41Today I conclude discussion of an e-mail correspondence I recently had with a financial adviser. What she said about a lack of peer-review in the industry has been quite the eye-opener for me.

> And then, take it one step further and pretend that

> you are not the investor, and instead are an advisor

> for a relatively unsophisticated (in the field of

> finance) client (or 200-300+ people as is usually

> the case). Which would you rather be responsible for

> advising a client to do… or, would you choose some

> other option that you have available? Keep in mind

> that advisors bear responsibility, not just legally,

> but personally (emotionally) for knowing that they

> may lose their clients’ retirement, education, or trust

Having so many clients is no excuse for using sub-optimal investment methods—methods that any individual could execute for him/herself given a healthy dose of education.

With regard to options, I have heard advisers complain about the excessive time/cost it would take to get regulatory clearance. Perhaps regulators are somewhat behind the curve but I’m not convinced. Some investment advisers do employ option strategies for their clients. Given my belief that many advisers don’t know options I wonder if those complaining have even tried? And if the compliance firm is to blame then find one that is option-friendly!

> money. And, remember that they have to implement their

> investment strategy for not just one or two families, but

> hundreds. Given these conditions, do you think advisors

> will be overly risk-averse (compared to the purely

> logical choice they might otherwise make based on

> economics) in their decision making? Statistical inference

> matters less to investors/clients who have lost any

> percentage of wealth, especially if they don’t fully

> understand why the risks were taken/decisions made.

To me, the omission of statistical significance is like off-label drug usage. Physicians occasionally prescribe medication for reasons not mentioned in the package labeling. If this is not standard of practice and if peer-reviewed data do not support said off-label indication then the physician could be susceptible to legal action should adverse events occur.

Given that evidence-based medicine has done well to advance medical practice in this country, why aren’t financial advisers held to the same standard? Do good statistical research that can be authenticated and replicated and use those methods to manage money for the public. Without this, I struggle to view the financial industry as delivering anything more than quackery to unsuspecting retail clients.

Categories: Financial Literacy | Comments (0) | PermalinkPerspectives of a Financial Adviser (Part 4)

Posted by Mark on December 15, 2016 at 07:22 | Last modified: September 14, 2016 05:13I feel I sometimes give financial advisers short shrift so I decided to do a blog series focusing on the words of one adviser who I respect. It hasn’t been going well.

> My previous points about compliance and legal

> concerns are intended to highlight the idea

> that even if he wanted to include a statement

> about [statistical] significance, he couldn’t

> because it would be an overstatement of

> confidence/create more misunderstanding

> among relatively uneducated readers than is

> acceptable by industry standards.

As stated previously, I believe statistical significance is necessary to evaluate the possibility of fluke occurrence. I also think this allows for apples-to-apples comparison with other statistically significant data. Since the author is the only one capable of doing the analysis, why not include a disclaimer(s) that clears the way for statistical reporting?

> I know it’s frustrating not to be able to apply

> experimental methods directly in this field, and

I disagree. I think it is possible to undertake the laborious task of trading system development but most advisers/traders are not educated about the methodology and/or capability of the process.

> to some degree it is that frustration and lack of

> predictability that compels people to work with an

> advisor. Sometimes this is because they feel that

> someone with more experience and education would

> be able to take better bets than they would, but

> sometimes it is because they want to outsource the

> stress of the unpredictable returns. They want

> someone to take the blame (other than themselves)

> if their portfolio doesn’t do what they want it/expect

> it to, which is inevitable at some point. Both of

She makes really good points here.

> these reasons to work with an advisor are

> legitimate, and on top of those, concerns about

> continuity and consolidation of household wealth

> mean that individuals rarely manage their own

> portfolios/trusts for their entire lives. At some

> point, they decide that someone else should be

> the fiduciary keeper of that burden/process/role.

My dispute is with what people don’t know they don’t know. The cost to offload said burden amounts to much more than the 1% (or less) management fee because most advisers employ relatively inconsistent investment vehicles.

I will conclude with the next post.

Categories: Financial Literacy | Comments (1) | PermalinkPerspectives of a Financial Adviser (Part 3)

Posted by Mark on December 13, 2016 at 06:48 | Last modified: January 25, 2018 09:32I have been presenting some excerpts from an e-mail correspondence I had with a financial adviser a few months ago.

She continued:

> The status quo is to calculate the return by

> acceptable methods… and report it “as is” for

> investors or advisors to interpret as they see fit.

I would argue without knowledge of statistics and system development, neither investors nor advisers are in any position to interpret that return. The adviser is usually the one left to do the interpretation and I can only hope s/he has a thorough understanding of scientific methods and statistical testing like those publishing in peer-reviewed journals.

> …I’m not suggesting that he cherry-picked returns.

> He cited his sources in the usual way (where the raw

> data came from, and that it was manipulated). This is

> all that is required to be in compliance… This

> strategy avoids the appearance of overstating the

> performance as [statistical] significance might do for

> readers who don’t understand the limitations of

> [statistical] significance. It’s the job of the

> compliance officer and the publishers of the magazine

> to protect… from law suit[s]. “Average” is perceived

> as a less complex and therefore less dangerous term.

> Averages don’t assert anything, they simply get

> reported, and readers make meaning for themselves.

> “Significance” is a term that may implicitly overstate

> findings to a degree that may mislead unsophisticated

> readers, putting the writer/magazine at risk.

This was shocking to me. Advisers should not publish statistical analysis because they may overstate importance to the uneducated reader? In my opinion, statistical analysis is necessary to suggest a difference might be meaningful. And only the author can do the statistical analysis since the entire data set is rarely (if ever) presented in the article itself.

> This fear of overstatement runs through everything

> from professional signatures to performance reporting.

> Implied guarantees or overstatement are very common

> compliance concerns across the industry. It would be

> for these reasons that I would guess Craig kept his

> calculations so simple…

This tells me that the compliance officers give advisers (authors) carte blanche to publish anecdotal information rather than statistically tested, validated data. It’s like optionScam.com everywhere. I find this extremely disconcerting…

…but I will continue next time, nonetheless.

Categories: Financial Literacy | Comments (0) | Permalink